Structural Drivers of Growth at Risk:

Insights from a VAR-Quantile Regression approach

ECB Working Paper (Podcast)

Together with Giacomo Carboni, Luìs Fonseca, and Fabio Fornari

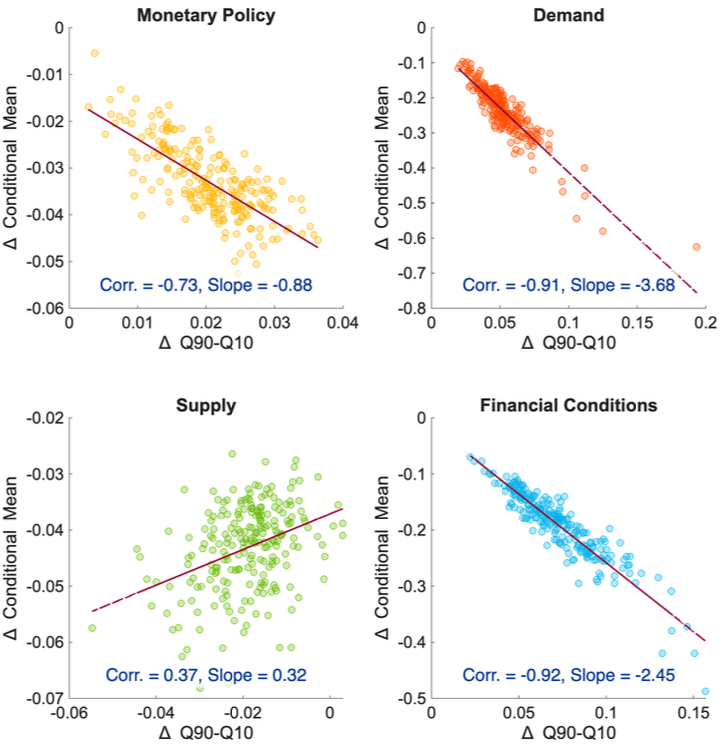

We investigate the impact of structural shocks on the joint distribution of future real GDP growth and inflation in the euro area. We model the mean of their distribution, together with selected financial indicators, using a VAR and perform quantile regression on the VAR residuals to estimate the time-varying variance as a function of macroeconomic and financial variables. Through impulse response analysis, we find that demand and financial shocks reduce expected GDP growth and increase its conditional variance, leading to negatively skewed future growth distributions. By enabling this mean-volatility interaction, demand-type shocks drive a significant time variation in downside risk to euro area GDP growth. Conversely, supply-type shocks do not generate the same mean-volatility interaction, resulting in symmetric movements in GDP growth and inflation quantiles.

Barking up the Wrong Tree? Climate News and Financial Stability

Current working paper (PDF)

Podcast (short/long)

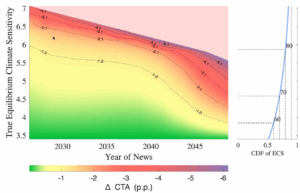

Uncertainty about climate change persists because key parameters in climate models remain poorly constrained. One of the most notable of these is equilibrium climate sensitivity (ECS) — the long-term increase in global temperature following a doubling of CO2. Using a New-Keynesian integrated assessment model with financial frictions, we investigate whether news shocks that update beliefs about ECS could cause the macro-financial system to become unstable. Due to their exceptional forward-looking nature, financial markets are especially vulnerable to information about the future. As such news arrives, agents revise their expectations, adjusting their behaviour, policy implementation and investment choices simultaneously. Therefore, we establish a direct link between the physical and transition risks of climate change and a single pivotal parameter. We find that bad news about ECS can trigger financial stress. It is transition risk — the attempt to limit climate change to 2°C — that causes this instability; physical risk itself does not generate significant financial stress in the short term. However, since those bad news lead to a decrease in the future real interest rate, supporting asset prices, especially the near term physical and transition risk to the financial market is limited.

Perturbation-Anchored Neural-Network Solutions of

Nonlinear DSGE Models

Very very preliminary draft (PDF)

This paper studies a perturbation-anchored neural-network workflow for solving nonlinear DSGE models. Nonlinear DSGE models are difficult to solve globally when the state vector is high-dimensional, expectations are forward looking, and occasionally binding constraints create nonsmooth policy rules. The method represents policy functions directly by neural networks and trains them to minimize nonlinear equilibrium residuals on sampled states. To discipline equilibrium selection, the loss includes long-run stability penalties and, in the New Keynesian applications, a local first-order perturbation anchor computed in Dynare. The workflow is evaluated in three environments: a deterministic Ramsey economy, a stochastic New Keynesian model with capital accumulation and adjustment costs, and a New Keynesian model with irreversible investment formulated as an occasionally binding complementarity constraint. Across the reported validation regions, the perturbation anchor helps the neural network remain on the economically relevant local branch, while nonlinear residual training improves equation accuracy away from the immediate steady-state neighborhood. In the irreversible-investment model, the complementarity residual allows the same policy-function approximation to represent both interior and constrained states.